Investor opinion

🫧 AI Companies' Shared Destiny Recalls Dot-Com Bubble Memories

Oswarld · 06/07/2026, 11:28 AM · Views 1,192

Oswarld · 06/07/2026, 11:28 AM · Views 1,192🌐 Auto-translated from Korean

Community of Shared Destiny in AI Infrastructure

The next opportunity after Nvidia is not in GPUs, but in bottlenecks

An interesting scene is emerging in the AI infrastructure market recently. Beyond simply "there aren't enough GPUs" or "more data centers are needed," a structure where giant corporations invest in each other, buy each other's services, and generate each other's revenue is growing.

This is also why the recent SpaceX issue is causing controversy in the market. SpaceX is reportedly nearing an IPO and has signed a large-scale AI computing lease agreement with Google, as well as a separate agreement with Anthropic. The Google contract is reported to be worth $920 million per month, and the Anthropic contract $1.25 billion per month, totaling approximately $26 billion in annual AI computing revenue from the two contracts combined.

On the surface, this suggests strong demand for AI computation. However, the market's discomfort lies elsewhere. There is a question of whether these transactions represent genuine external demand, or if they are structured to make revenue and corporate value look good ahead of an IPO.

My core point is this:

AI infrastructure investment is no longer a simple CAPEX competition, but is moving towards a community of shared destiny where big tech, AI model companies, GPU supply chains, cloud providers, and capital markets support each other.

And as this structure grows, the investment perspective needs to shift slightly. Instead of just looking at "who sells the most GPUs," we must also consider the bottlenecks that are absolutely necessary for those GPUs to actually operate: power, cooling, substrates, memory, optical communication, testing, and server assembly.

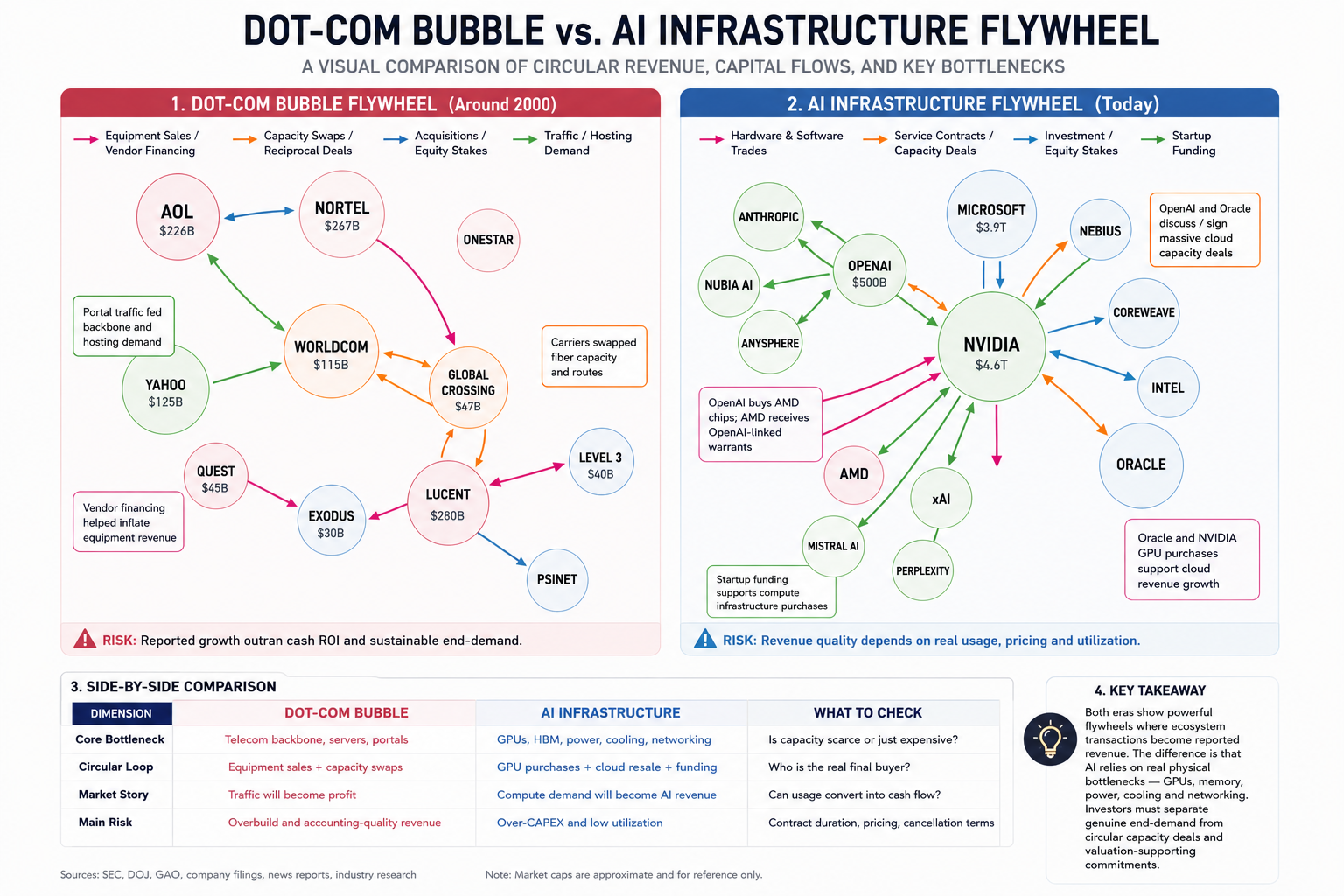

1. Why the AI Infrastructure Market Appears Cyclical

Looking at the current structure of the AI industry, $NVDA Nvidia is at the center. $NVDA supplies GPUs, and cloud companies purchase those GPUs in large quantities. AI model companies then lease cloud computing. And big tech invests in or holds stakes in AI startups, while simultaneously selling cloud services to them.

This structure itself is not necessarily problematic. Such things often happen in nascent industries. During the dot-com bubble, equipment manufacturers, portals, telecommunication companies, hosting companies, and internet companies grew by generating revenue for each other.

The problem is that at some point, it becomes difficult to distinguish between genuine end-user demand and internal ecosystem transactions.

| Category | Dot-com Bubble Era | Current AI Infrastructure |

|---|---|---|

| Key Bottleneck | Communication networks, servers, portal traffic | GPUs, power, data centers, memory |

| Central Companies | Cisco, AOL, Yahoo, WorldCom | $NVDA, $MSFT, $GOOGL, $AMZN, $ORCL |

| Cyclical Structure | Equipment sales → Traffic increase → Additional investment | GPU purchase → Cloud leasing → AI revenue recognition |

| Investor Question | Does traffic translate into money? | Does AI usage translate into actual revenue? |

| Risks | Overcapacity, accounting revenue inflation | Excessive CAPEX, internal transaction-driven demand, low ROI |

The recent SpaceX case, viewed from this perspective, is not just a simple "AI computing contract." As SpaceX aims to incorporate space data center and AI computing businesses into its IPO story, the fact that major clients like Google and Anthropic have signed long-term contracts is certainly positive.

However, at the same time, we must consider the contract unit price, the possibility of early termination, actual GPU supply conditions, and the connection to the internal ecosystem. Especially for a company nearing an IPO, the quality of revenue is as important as the sheer volume of revenue.

2. $NVDA is Ultimately at the Center of This Controversy

The most important company in this trend is still $NVDA Nvidia.

$NVDA is not just a company that sells GPUs. In the current AI infrastructure market, it is virtually the "standard unit of computing power." Google, Microsoft, Amazon, Oracle, CoreWeave, xAI, Anthropic, and OpenAI are all ultimately competing for GPU acquisition.

Even in the recent SpaceX contracts, the core issue is "who pays how much to secure what computing resources." The Google contract reportedly includes access to a large number of Nvidia GPUs and related infrastructure, and the Anthropic contract is also linked to the right to use a large number of Nvidia chips in Colossus data centers.

Therefore, the investment thesis for $NVDA remains strong. However, at the same time, the questions must change.

The old question was:

"How much more will Nvidia sell if AI demand increases?"

Now, the question is shifting to:

"Can customers who bought Nvidia GPUs generate sufficient profits?"

This difference is crucial. Strong GPU demand is one thing; whether companies that purchase GPUs can recoup their investment is another. During the dot-com bubble, equipment demand was real. The problem was that the traffic generated by that equipment did not translate into sufficient cash flow.

$NVDA remains the strongest bottleneck in the AI supply chain. However, a good company and a good price are different. Especially if the market starts to price in the entire AI infrastructure investment as "naturally profitable," the risks might emerge first not with GPU selling companies, but with companies leasing GPUs or those buying GPUs at high prices to lease them out.

3. What We Really Need to Look At Is the "Quality of AI Revenue"

In this controversy, what investors should focus on is not the contract size itself. What matters is the quality of revenue.

When an AI infrastructure company announces a large contract, at least four things should be examined:

| Checklist Item | Reason to Look |

|---|---|

| Who is the customer? | Verify if it's a genuine external customer, or an affiliate, investor, or internal ecosystem customer. |

| Is the contract terminable? | Even if it looks like a long-term contract, early termination clauses reduce revenue visibility. |

| Is the unit price consistent with market rates? | Abnormally high unit prices can raise suspicions of accounting revenue inflation. |

| Is there end-user demand? | Confirm if cloud leasing demand is actually translating into AI product revenue. |

In SpaceX's case, there are certainly arguments in its favor. Securing initial utilization rates is important for AI data centers, and the involvement of customers like Google or Anthropic could signal the quality and demand for those computational resources.

However, conversely, for a company nearing an IPO, investors are most sensitive to such internal circular structures when a large AI revenue story is being built. While revenue may appear large, it's crucial to determine whether it represents genuine external cash flow or a structure where ecosystem participants mutually support each other's valuations.

During the dot-com bubble, the internet was real. Traffic was real, and demand for servers and network equipment was real. What was wrong was not the direction, but the speed and the price. AI is similar now. It's hard to doubt that AI is a massive transformation. However, it doesn't mean that all AI infrastructure investments will yield good returns.

4. Related Stocks Should Be Divided by Bottleneck, Not Just Market Leaders

In this trend, simply concluding with "it's AI, so $NVDA" would be a bit insufficient. As the AI community of shared destiny structure grows, bottlenecks expand from GPUs to data centers, power, cooling, memory, networks, and cloud leasing providers.

| Theme | Key Stocks | Reason to Look |

|---|---|---|

| GPU·AI Accelerators | $NVDA, $AMD | Direct beneficiaries of AI computing demand |

| Cloud·AI Infrastructure | $MSFT, $GOOGL, $AMZN, $ORCL | Absorb computational demand from AI model companies |

| AI Data Center Leasing | $CRWV | Representative case of GPU leasing and AI cloud demand |

| Memory·HBM | $K000660 SK Hynix, $K005930 Samsung Electronics, $MU | Memory bottleneck due to AI server expansion |

| Power·Cooling | $ETN, $VRT, $E:SU | Physical bottleneck of data center expansion |

| Network·Optical Communication | $AVGO, $ANET, $COHR | Data movement bottleneck due to GPU cluster expansion |

Companies like $CRWV CoreWeave are directly relevant to this discussion. Their model involves acquiring large quantities of GPUs and leasing AI computing power. When demand is strong, leverage works significantly, but conversely, if unit prices fall or utilization rates decrease, profitability risks can also increase.

$ORCL Oracle is also in an interesting position. While it appears to be a traditional software company, it has recently become deeply involved in AI cloud infrastructure demand and the competition to secure large-scale GPU clusters. However, here too, "margin and payback period" must be considered alongside "order volume."

In Korea, $K000660 SK Hynix and $K005930 Samsung Electronics remain key players. As AI infrastructure competition continues, demand for HBM and high-performance memory will structurally increase. However, market expectations for these companies are already high, so the pace of earnings upgrades and the pace of price reflection should be considered separately.

5. What $NVTS Showed: AI Bottleneck Is Shifting to Power

The reason $NVTS Navitas recently gained market attention is also linked to this trend. The core point is not simply "an Nvidia-related stock." It's because as AI data centers scale up to rack units, power conversion, power density, and high-efficiency power supply are emerging as new bottlenecks.

After Nvidia's GB200 and GB300, AI infrastructure is no longer a matter of adding a few servers. Entire racks operate like a single giant computing system, and within that, GPUs, CPUs, HBM, networking, cooling, and power must all be optimized simultaneously.

In this trend, $NVTS garnered market interest with its GaN/SiC-based power semiconductors and 800V DC power architecture story. The important point is not just $NVTS itself, but the signal that the next bottleneck in AI data centers is shifting to power.

Therefore, when looking at Chinese, Japanese, and Taiwanese stocks, it seems better to approach it not by "do they directly supply Nvidia," but by "what are the absolutely necessary bottlenecks as Nvidia's AI factories grow?"

6. Taiwan: The Most Direct AI Server, Power, and Cooling Supply Chain

Taiwan remains the most crucial region in the AI infrastructure supply chain. $TSM TSMC is at the core of Nvidia's AI chip manufacturing and advanced packaging, and below that are AI server ODM, power, cooling, connector, and cable companies.

Rack-scale systems like Nvidia's GB200 NVL72 do not operate with GPUs alone. Who builds the rack, who supplies the power, and who removes the heat are all critical. This is where Taiwanese companies are strongly connected.

| Category | Stocks of Interest | Reason to Look |

|---|---|---|

| Foundry·Packaging | $TSM / $TW2330 TSMC | Nvidia AI chip manufacturing and CoWoS bottleneck |

| AI Server ODM | $TW2382 Quanta, $TW3231 Wistron, $TW6669 Wiwynn, $TW2317 Foxconn | GB200/GB300 rack server assembly·system integration |

| Power·Cooling | $TW2308 Delta Electronics | 800V DC, power racks, CDUs, modular AI data centers |

| Connectors·Cables | $TW3665 BizLink | Demand for high-power·high-speed interconnects |

| Cooling Components | $TW3324 Auras, $TW3017 Asia Vital Components | Liquid cooling·thermal management bottleneck |

Among these, the cleanest candidate is $TW2308 Delta Electronics. If $NVTS represents the 800V DC power conversion story in the US, Delta is the most similar "AI data center power bottleneck" perspective in Taiwan.

Delta is not just a power supply company. It has expanded into data center power infrastructure, power racks, cooling solutions, and CDUs. As AI data centers become denser, the importance of companies that handle both power and cooling will inevitably grow.

$TW6669 Wiwynn is also interesting. It specializes more in data center servers than general PC/laptop ODM, so it has high sensitivity to the proliferation of AI server racks. However, since it is already widely recognized as a leading AI server stock in the market, valuation burden must be considered alongside it.

7. Japan: Bottlenecks in Equipment, Substrates, Materials, and Measurement

Japan seems to be a better fit for semiconductor equipment, substrates, materials, measurement, and optical fiber rather than finished products. As AI semiconductors become more complex, "manufacturing equipment," "attaching substrates," "testing equipment," and "connecting materials" become more important.

| Category | Stocks of Interest | Reason to Look |

|---|---|---|

| Substrates | $J4062 Ibiden | AI chip package substrate bottleneck |

| Testing | $J6857 Advantest | AI/HPC semiconductor testing demand |

| Cutting·Polishing | $J6146 DISCO | Advanced packaging·post-processing precision machining |

| Optical Fiber·Power Cables | $J5803 Fujikura | Data center network·power infrastructure |

| Electronic Components | $J6981 Murata, $J6762 TDK | Demand for power·passive components·high-frequency components |

| Ceramics·Materials | $J5332 TOTO, $J5333 NGK Insulators | Ceramics·components for semiconductor equipment |

Here, $J4062 Ibiden can be viewed most directly as part of the Nvidia supply chain. AI chips are not just about the GPU. HBM, interposers, and package substrates must all go together. As high-performance AI chips become larger and more complex, the importance of high-performance package substrates also increases.

$J6857 Advantest is also an important candidate. AI/HPC chips are expensive and complex in structure, making testing difficult. As the price of a single chip increases, the value of testing equipment that catches defects also rises. This company is not a market leader, but rather an approach to view the measurement and testing bottleneck that becomes necessary as AI semiconductors advance.

Looking a bit broader, $J5803 Fujikura is also worth considering. This is because the AI data center bottleneck is moving beyond power and cooling to optical communication. As GPU clusters grow, the amount of data movement increases, which is linked to demand for optical fiber, cables, and high-speed network infrastructure.

8. China: Alternative Supply Chains·Optical Communication Rather Than Direct Nvidia Beneficiaries

China needs to be viewed a bit differently. Due to US semiconductor export regulations to China, it is difficult to find stocks directly integrated into Nvidia's cutting-edge GPU supply chain. Therefore, it's more appropriate to view China in two directions rather than as "Nvidia beneficiaries."

First, the localization of AI infrastructure within China. Second, optical communication, power, and server components that go into global data centers.

| Category | Stocks of Interest | Reason to Look |

|---|---|---|

| Optical Modules | $S300308 Zhongji Innolight | AI data center optical transceiver demand |

| Optical Modules | $S300502 Eoptolink | High-speed optical communication modules |

| Optical Communication | $S002281 Accelink | Optical components·modules |

| Servers·Manufacturing | $S601138 Foxconn Industrial Internet | AI server·cloud infrastructure manufacturing |

| China GPU·AI Chips | $S688256 Cambricon, $S688041 Hygon | Localization of AI semiconductors within China |

| Foundry | $H00981 SMIC, $H01347 Hua Hong | Key infrastructure for China's semiconductor self-reliance |

Among Chinese stocks, the closest to the "AI data center bottleneck" are optical modules. Companies like $S300308 Zhongji Innolight and $S300502 Eoptolink can gain attention as data movement between servers increases with larger GPU clusters.

However, many Chinese optical module stocks have already priced in significant AI beneficiary expectations. Therefore, rather than simply viewing them as "AI data center beneficiaries," actual revenue growth rates and valuations must be considered together.

From the perspective of China's semiconductor localization, $S688256 Cambricon, $S688041 Hygon, and $H00981 SMIC can also be included in the candidate group. However, these are less about Nvidia benefits and more about alternative demand arising in markets where Nvidia cannot be used. Thus, the investment logic is entirely different. They involve significant technology gaps, sanction risks, and reliance on government policy.

Summary from an Investment Perspective

The recent SpaceX controversy and the surge in $NVTS are not isolated issues. Both point in the same direction.

The AI infrastructure market can no longer be explained by GPUs alone. While $NVDA is at the center, as the number of GPUs increases, bottlenecks expand to power, cooling, memory, substrates, testing, optical communication, server assembly, and cloud leasing structures.

Therefore, from an investment perspective, two questions must be considered together:

First, does this revenue come from actual usage by end customers, or is it a transaction within the AI ecosystem that supports each other's growth?

Second, where is the absolutely necessary bottleneck shifting as AI grows?

Considering these two questions together reveals a much broader map than simply whether or not to buy $NVDA.

| Theme | Key Stocks | Reason to Look |

|---|---|---|

| GPU·AI Accelerators | $NVDA, $AMD | Center of AI computing demand |

| AI Cloud | $MSFT, $GOOGL, $AMZN, $ORCL, $CRWV | Convert GPU infrastructure into service revenue |

| Power Semiconductors | $NVTS | 800V DC, GaN·SiC-based power conversion story |

| Taiwan Power·Cooling | $TW2308 Delta Electronics | AI data center power·cooling bottleneck |

| Taiwan AI Servers | $TW6669 Wiwynn, $TW2382 Quanta, $TW3231 Wistron | Rack-scale AI server assembly·integration |

| Japan Substrates·Testing | $J4062 Ibiden, $J6857 Advantest | Package substrate and AI/HPC testing bottleneck |

| Japan Optical Communication·Components | $J5803 Fujikura, $J6981 Murata, $J6762 TDK | Data center network·power component demand |

| China Optical Modules | $S300308 Zhongji Innolight, $S300502 Eoptolink | AI cluster high-speed data movement bottleneck |

| China AI Localization | $S688256 Cambricon, $S688041 Hygon, $H00981 SMIC | Demand for alternative supply chains amidst sanctions |

| Korea HBM·Memory | $K000660 SK Hynix, $K005930 Samsung Electronics | Memory bottleneck due to AI server expansion |

If I had to choose one from each country, this is how I would see it now:

| Country | Top Candidate | Reason |

|---|---|---|

| Taiwan | $TW2308 Delta Electronics | Closest power·cooling bottleneck to $NVTS |

| Japan | $J4062 Ibiden | AI chip package substrate bottleneck |

| China | $S300308 Zhongji Innolight | AI data center optical communication bottleneck |

| Korea | $K000660 SK Hynix | HBM-centric memory bottleneck |

For a more stable large-cap combination, $NVDA, $TSM, $TW2308 Delta, $J6857 Advantest, $J4062 Ibiden, $K000660 SK Hynix would be good. For a more aggressive approach, $NVTS, $CRWV, $TW6669 Wiwynn, $TW3324 Auras, $S300308 Zhongji Innolight, $S300502 Eoptolink would be the direction.

Conclusion

Ultimately, what this trend shows is one thing: the AI industry is no longer about individual company competition, but is moving as a massive community of shared destiny. $NVDA sells GPUs, cloud companies buy them, AI model companies lease computing power, and investment and contracts mutually support each other's corporate valuations.

This structure acts as a powerful accelerator in the early stages of growth. However, at some point, it becomes necessary to distinguish the quality of revenue, the sustainability of contracts, and the reality of end-user demand.

At the same time, the AI infrastructure bottleneck does not end with GPUs. It continues to spread to power, cooling, substrates, memory, testing, optical communication, and server assembly. The recent attention on $MRVL and $NVTS is one scene in this trend. The market is now broadening the question from "who makes the AI chips" to "who actually makes the AI factory run."

Therefore, going forward, finding the absolutely necessary bottlenecks as AI grows may become more important than simply following the leading AI stocks. However, a good company and a good price are different. We are now in a phase where we need to assess not "is AI real?" but "how high-quality is AI revenue, and does that bottleneck actually translate into cash flow?"

This post reflects the author’s own opinion and is not investment advice or a solicitation from bullbear.ninja.